All Categories

Featured

Table of Contents

Getting rid of representative settlement on indexed annuities enables for significantly higher detailed and real cap rates (though still substantially reduced than the cap rates for IUL plans), and no question a no-commission IUL plan would push illustrated and actual cap prices higher. As an apart, it is still possible to have a contract that is really rich in agent settlement have high early cash money abandonment values.

I will yield that it goes to the very least theoretically POSSIBLE that there is an IUL policy available released 15 or 20 years ago that has provided returns that are exceptional to WL or UL returns (more on this below), however it is essential to much better comprehend what a proper comparison would involve.

These plans generally have one bar that can be evaluated the company's discernment each year either there is a cap rate that specifies the optimum attributing rate because certain year or there is an engagement rate that specifies what portion of any type of favorable gain in the index will be passed along to the policy in that specific year.

And while I normally agree with that characterization based upon the mechanics of the policy, where I differ with IUL proponents is when they identify IUL as having remarkable returns to WL - no load universal life insurance. Several IUL advocates take it an action additionally and indicate "historical" data that appears to sustain their insurance claims

Initially, there are IUL plans around that lug more risk, and based upon risk/reward principles, those plans need to have greater expected and actual returns. (Whether they actually do is a matter for significant dispute however business are using this technique to aid warrant greater detailed returns.) Some IUL plans "double down" on the hedging method and analyze an added charge on the plan each year; this charge is then utilized to enhance the options spending plan; and after that in a year when there is a positive market return, the returns are enhanced.

Equity Indexed Universal

Consider this: It is possible (and as a matter of fact most likely) for an IUL policy that averages an attributed rate of say 6% over its first ten years to still have a total negative price of return throughout that time because of high costs. A lot of times, I find that representatives or customers that extol the efficiency of their IUL plans are puzzling the attributed rate of return with a return that appropriately shows all of the plan charges as well.

Next we have Manny's inquiry. He says, "My pal has actually been pushing me to buy index life insurance and to join her company. It looks like a network marketing. Is this a good concept? Do they truly make how much they say they make?" Allow me begin at the end of the inquiry.

Insurance policy salespersons are okay individuals. I'm not recommending that you 'd dislike on your own if you said that. I claimed I used to do it, right? That's how I have some understanding. I used to sell insurance coverage at the beginning of my occupation. When they offer a costs, it's not unusual for the insurer to pay them 50%, 80%, even in some cases as high as 100% of your first-year premium.

It's difficult to sell due to the fact that you got ta always be looking for the next sale and going to locate the following individual. It's going to be difficult to discover a lot of fulfillment in that.

Let's talk about equity index annuities. These points are preferred whenever the markets are in a volatile period. You'll have abandonment periods, usually seven, ten years, possibly even past that.

Universal Benefits Insurance

Their abandonment periods are huge. So, that's how they understand they can take your money and go completely spent, and it will certainly be okay because you can't obtain back to your cash until, once you're right into seven, 10 years in the future. That's a lengthy term. No issue what volatility is taking place, they're possibly going to be fine from an efficiency perspective.

There is no one-size-fits-all when it comes to life insurance coverage. Obtaining your life insurance coverage strategy best takes into consideration a number of elements. [video description: Pleasant music plays as Mark Zagurski speaks to the camera.] In your busy life, financial freedom can look like a difficult objective. And retired life might not be leading of mind, due to the fact that it appears up until now away.

Pension, social protection, and whatever they would certainly handled to save. It's not that very easy today. Fewer companies are using conventional pension and several firms have actually minimized or terminated their retirement and your capability to count exclusively on social security remains in question. Even if benefits have not been lowered by the time you retire, social safety alone was never ever planned to be sufficient to spend for the way of living you desire and are entitled to.

The Cash Value In An Indexed Life Insurance Policy

/ wp-end-tag > As component of an audio financial approach, an indexed universal life insurance policy can assist

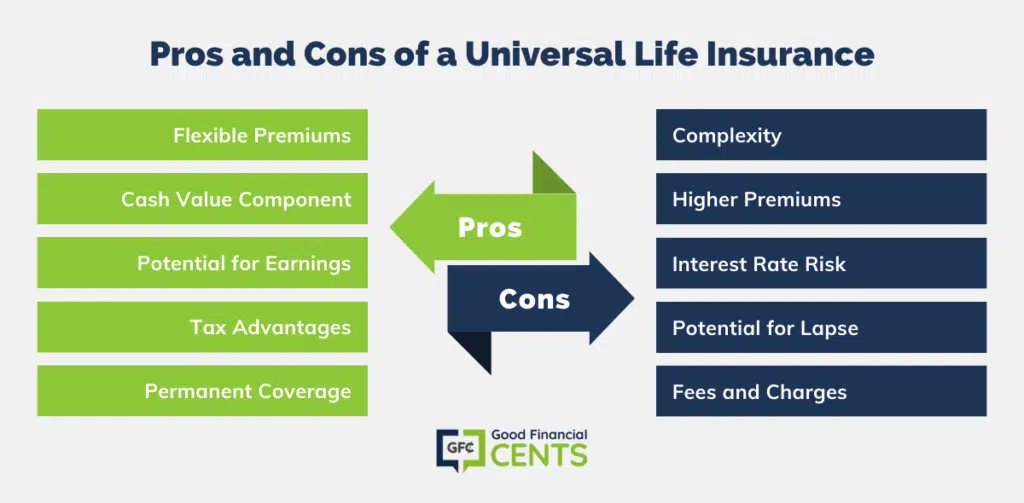

you take on whatever the future brings. Prior to dedicating to indexed global life insurance, here are some pros and cons to think about. If you pick a good indexed universal life insurance policy plan, you might see your cash money worth expand in worth.

Because indexed universal life insurance policy calls for a specific degree of risk, insurance coverage firms tend to keep 6. This kind of strategy additionally uses.

Lastly, if the picked index does not do well, your money worth's development will be affected. Typically, the insurance policy firm has a beneficial interest in carrying out far better than the index11. There is typically an assured minimum interest price, so your plan's growth won't fall listed below a certain percentage12. These are all factors to be taken into consideration when choosing the most effective kind of life insurance coverage for you.

However, because this kind of plan is more complicated and has an investment component, it can often include higher costs than other policies like entire life or term life insurance. If you don't believe indexed global life insurance is right for you, below are some alternatives to consider: Term life insurance policy is a temporary plan that normally uses protection for 10 to thirty years.

Nationwide Single Premium Ul

When determining whether indexed global life insurance policy is ideal for you, it's essential to consider all your alternatives. Entire life insurance might be a far better option if you are searching for more security and uniformity. On the other hand, term life insurance policy may be a better fit if you only require insurance coverage for a particular time period. Indexed universal life insurance is a kind of plan that offers much more control and versatility, along with higher cash value growth capacity. While we do not supply indexed universal life insurance policy, we can give you with even more information concerning entire and term life insurance policy policies. We recommend exploring all your options and talking with an Aflac representative to discover the very best fit for you and your family.

The remainder is added to the money value of the policy after charges are deducted. The cash worth is attributed on a month-to-month or yearly basis with passion based upon boosts in an equity index. While IUL insurance may verify beneficial to some, it is necessary to comprehend exactly how it works prior to purchasing a plan.

{kind=link}

Table of Contents

Latest Posts

Equity Index Insurance

Iul Vs Term Life

Iul 保险

More

Latest Posts

Equity Index Insurance

Iul Vs Term Life

Iul 保险